You must have heard people ask, how well can a business meet its financial obligations, and more so, their short-term ones? This question is asked often and the answer it leads to is pretty straightforward. It is the concept of liquidity ratio.

In simple words, it is a measurement that is primarily used to understand a business’s ability to fulfill its immediate debts by using the existing assets. It just shows how quickly a company can settle its short-term liabilities by making a swift conversion of its assets to cash.

A greater liquidity ratio, which reflects stability and sound financial standing, indicates that the company is in a better position to meet its present commitments. But, what exactly is it, and how do you calculate it? That’s what we are here to answer. Continue reading this blog post to learn everything in detail.

Types of Liquidity Ratios

Before understanding how to calculate liquidity ratio, you should definitely have a basic idea about its types. This can make it even simpler to decipher liquidity ratios. So, here we go:

1. Current ratio

This is typically the broadest measure that classifies your business’s financial obligations, comparing its current assets against the current liabilities. On the whole, it offers a very general view. That being said, this is generally beneficial for different types of businesses but not exactly a great worker if we look at companies in the same industry.

2. Cash ratio

As the name suggests, this analyzes whether a company is competent enough to cover its current liabilities using its cash and cash equivalents. Learn about Free Cash Flow here. Now, if you ask whether both current ratio and cash ratio are the same – then the answer is no. There is a simple reason behind it. Unlike the current ratio, the cash ratio is known to take cash and cash equivalents into account. This is part of the reason why it is often called a conservative liquidity measure.

3. Acid test ratio (quick ratio)

This can be usually considered between the current and cash ratios. That is because the Acid Test Ratio caters for cash and its equivalents (which are part of the cash ratio formula), among marketable securities and receivable accounts. But, in the meantime, it also excludes inventory and prepaid expenses. That goes to show how it focuses more on liquid assets.

4. Operating cash flow ratio

In simple words, this is a measure that shows how well a business’s regular cash-producing activities can fulfill its short-term debts. In this ratio, cash from operations is more favored over net income for the business. In other words, it basically looks at actual cash flow and not just the profit numbers.

Now that you know its types, it is time to understand how to calculate a liquidity ratio. So, without further ado, let’s get into it.

Need help with different liquidity ratios?

Consult our accounting experts.

How to Calculate Liquidity Ratios?

To understand how to calculate liquidity ratio, we need to have a look at all the liquidity ratio formulas and then grasp the concept of their calculations.

Current Ratio Formula

Here is the formula of current ratio:

Current Ratio = Current Assets / Current Liabilities

In this case, the current assets house all the current assets, which typically include accounts receivable, inventories, cash, and cash equivalents, among several other current assets.

On the flip side, current liabilities, as the name indicates, house all liabilities that are to be paid within an accounting timeframe. This broadly includes wages, debts, interest payments, and taxes due, among several other accrued expenses, such as rent and legal settlements (if any). Furthermore, it includes long-term liabilities as well that are also payable in the ongoing accounting year.

Cash Ratio Formula

Here is the formula of cash ratio formula:

Cash Ratio = Cash and Cash Equivalents / Current Liabilities

Unfortunate times always come unannounced. During times of recession or other economic upheaval, you must have cash on hand to handle these emergency expenses.

Looking at its numerator, the cash ratio takes into account (which are the in-hand cash material, along with what’s in the bank) and cash equivalents (which can be bills of exchange). Moreover, it leaves out all other liquid assets, such as accounts receivables and inventory. What else? A cash ratio of less than one indicates that the company does not have enough cash.

Quick Ratio Formula

Here is the formula of quick ratio:

Quick ratio = Quick Assets / Current Liabilities

For most businesses, quick assets can be limited to only a couple of assets. In that case, we have:

Quick Assets = Cash + cash equivalents + Marketable securities + Net accounts receivable

A company’s quick assets are basically cash or materials that can be quickly converted into cash. A company’s current assets may influence how it determines its quick assets. For instance, items like inventory and prepaid expenses are difficult to convert into cash. Thus, a business may evaluate its quick assets by deducting these slower-to-convert items from its total current assets. Henceforth, here is what it would look like:

Quick Assets = Total Current Assets – Inventory – Prepaid Expenses / Current Liabilities

Operating Cash Flow Ratio Formula

Here is the formula of operating cash flow ratio:

Operating Cash Flow Ratio = Cash from Operating Activities/ Current Liabilities.

The company’s cash flow statement shows the cash from operations. Cash from operating activities, on the other hand, shows the cash equivalent part of the net income.

Interpretation of Liquidity Ratios

Liquidity, in layman’s language, exhibits how easily your assets can turn into cash. Now, liquidity ratios are often the most useful when they are used in a comparative format. It can be either internal or external.

For internal comparisons, we generally have a closer look at the different timeframes using constant accounting practices. For the most part, this is a big help for analysts to understand how the business is changing over a certain time period. In general, a higher liquidity often indicates that the company can satisfy its debt quite swiftly.

For external comparisons, we generally have to take a closer look at one company’s ratios against others or, at times, the whole industry itself. It is incredibly beneficial to set benchmark goals and review the current standing of the company against its competitors. Nevertheless, comparing different industries at varied locations may not be beneficial due to their disparate financial requirements. Read more about Financial Benchmarking here.

Importance of Liquidity Ratio Analysis

If you didn’t know, liquidity ratio analysis is just as important as understanding how to calculate it. Here’s a detailed rundown of why:

A. Identifying potential financial risks

Liquidity ratio analysis can lend a helping hand in pinpointing risks that a company may encounter financially. When companies analyze this ratio, it becomes easier for them to convert assets into cash. This is especially important in times of rough financial obstacles. Moreover, a lower liquidity ratio is a big red flag as it indicates higher risk. In simple words, it shows that a business is actually struggling to pay off its debt right on time.

B. Supporting strategic planning and budgeting

Companies can usually make wise decisions about resource allocation, project investment, and budget structuring when they have a clear idea about liquidity positions. This helps them big time to maintain enough liquidity to sustain operations and growth.

Want help with strategic planning and budgeting?

Look no further! Get a free consultation session with our CFO

C. Assessing the ability to meet short-term obligations

One of the most integral parts of this ratio is to understand a business’s ability to cover its short-term obligations without the major distress that comes with it financially. Now, this can be anything between paying dues to suppliers and employees, along with several other short-term creditors. To keep stakeholders’ confidence and credibility, a company needs to be able to fulfill its commitments on time. If they happen to do it, then it means that the company comes with a fit liquidity ratio.

D. Evaluating financial performance and stability

Liquidity ratios basically give us a larger picture of how well a company is performing and whether it is in a stable condition. A consistent track of a company that has been maintaining a high liquidity ratio clearly tells us a lot more about how well they have been sustaining themselves in tough weather. Want to maintain long-term sustainability? Then, it is high time that your company starts to check on its financial well-being and gradually make adjustments as necessary. Know more about what is a financial audit and how to prepare for it

What is Liquidity Coverage Ratio?

In layman’s language, the liquidity coverage ratio is basically the percentage of highly liquid assets that financial institutions hold to make sure they can fulfill their short-term (i.e., 30-day cash outflow) obligations. You may ask, why 30 days? Well, 30 days was previously chosen because a response from governments and central banks, during a dire financial distress, would generally take almost a span of 30 days.

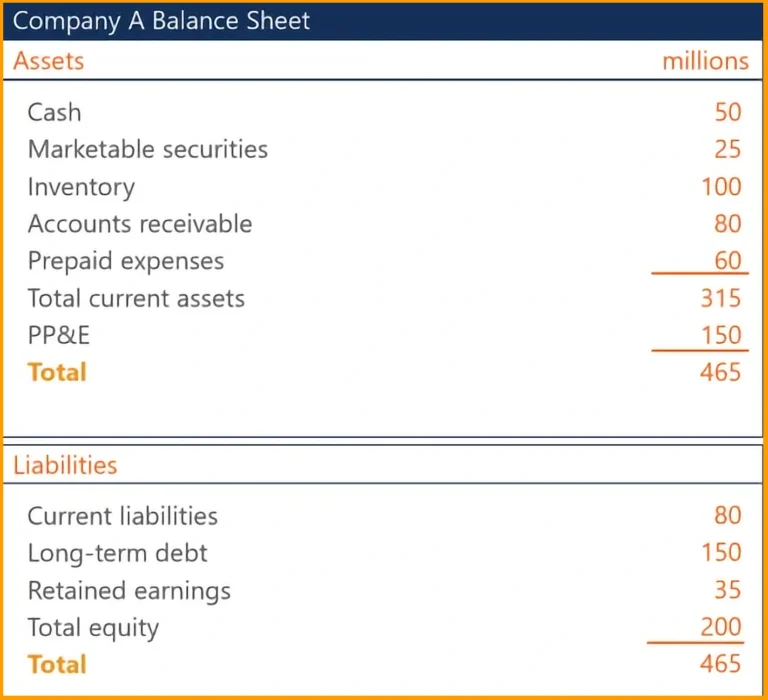

Case Study of Liquidity Ratio Example

Let’s assume “Company A” to understand whether they can pay off their short-term debts by using their existing assets. In this case, we will have to focus on the three most integral ratios, the Current ratio, Quick ratio, and Cash ratio – to learn liquidity ratio examples.

Now, Company A basically has:

1. $315 million in assets that can be converted into cash pretty quickly (such as, cash and its equivalents, stocks that can be sold, and money customers owe, among others).

2. $80 million is in debt, which needs to be repaid very soon.

3. The remainder of the balance sheet is actually composed of the company’s total investments and long-term debts.

Moving on, let’s analyze the liquidity of Company A.

Current Ratio

In this case, we can evaluate the current ratio when $315 million (i.e., current assets) is divided by $80 million (current liabilities).

→ Thus, $315 / $80 = 3.9

But, what does this even mean? In simple words, Company A already has $3.9 ready to go for every $1 it is going to pay soon. It is a very good sign, given the fact that they can easily handle immediate debts.

Quick Ratio

To estimate the quick ratio, this is what we have to do:

→ ($50 million in cash + $25 million in marketable securities + $80 million in accounts receivables) / $80 million as current liabilities

Therefore, $50 + $80 + $25 / $80 = 1.9

This means one very simple thing. Even when the company does not sell off its products (that is, its inventory), it still has $1.9 for every $1 of near-term debt. Truth be told, it is a favorable outcome and a healthy value.

Cash Ratio

In this case, the calculation is going to be:

→ ($50 million in cash + $25 million in marketable securities) / $80 million (which is, current debts).

If shown in plain values, we get:

Thus, $50 + $25 / $80 = 0.94.

But, what exactly does this suggest?

By pinpointing just cash and other closely related assets, Company A basically houses 94 cents for every $1 of debt. While it is a little under 1, it is still quite a good sign. This is because it shows that the business will not be too far from being able to settle its debts immediately with cash alone.

As a result, it goes to show that Company A is definitely in a good position. It has just enough in the pipeline to fulfill all its short-term debts, which is actually a pretty big green flag. This implies that potential investors or lenders are likely to have a favorable opinion of Company A.

What is a Good Liquidity Ratio?

When we say “good” liquidity ratio, then it must be anything higher than the value of 1. That being said, it is unlikely that a liquidity ratio of 1 will demonstrate that your company is worthy of investment. In general, a creditor or investor will potentially look for a liquidity ratio that is nothing less than 2 or 3. However, just so you know, the “ideal” liquidity ratio largely depends on the industry and the type of business you have.

Limitations of Liquidity Ratios

Just as much as there are so many bright sides, there will undoubtedly be limitations of liquidity ratios too. So, without further ado, let’s look at them:

A. Narrow focus on short-term liquidity: It is true that liquidity ratios are mainly responsible for analyzing a business’s ability to satisfy all its short-term financial obligations. The major problem here is that it may not be able to give you a complete, and A to Z perspective of the financial wellbeing of the company.

B. Ignoring qualitative aspects of liquidity: The quality and accessibility of assets, including the very speed at which inventory can be sold without a serious price decline, are actually not considered by this ratio. It is one of the major hurdles in this case.

C. Inability to predict future cash flows accurately: Without second guessing, liquidity ratios are mostly based on current or historical data. That is actually not enough to properly reflect the future cash flow a company may have.

In Wrapping up

When you are assessing a company’s financial stability, liquidity ratios do offer several noteworthy insights that are otherwise overshadowed by growth metrics and profit margins.

These ratios reveal a lot of answers to certain lingering questions we always have, such as: Can the company convert its assets into cash effectively? Does it have a strong defense against unforeseen financial difficulties? What is the liquidity ratio in relation to industry norms? This ratio shows a business’s capability to satisfy its immediate obligations. As a result, it is generally a massive help to understanding its potential risks and current financial cushion. Read more about credit risk management here.

This is enough proof of how important liquidity ratios can be, but it is advised not to base the total financial well-being of your company just on them. Always try to look beyond the shell because there are several areas to look at when you want a complete picture.

Need more information? We can help. Get in touch with experts who have more than 12 years of experience in this field.