- A general ledger is the central record of a company’s financial transactions and accounts.

- It covers assets, liabilities, equity, income, and expenses.

- GL codes uniquely identify and classify each financial transaction.

- Essential GL terms include debits, credits, chart of accounts, journal entries, and trial balance.

- Types of ledgers include traditional, tax, asset, expense, accounts payable, and receivable.

- Reconciliation ensures ledger accuracy.

- Best practices include clear accounts, regular entries, and scheduled audits.

A general ledger is a company’s financial command center, where all the penny that comes in and goes out is recorded thoroughly.

From purchases to bill payments, people consider it more as the heartbeat of a business’s financial operations.

But what exactly is it?

And why should you even care about it?

Here’s a detailed guide to the importance of general ledger and how it can impact your business.

What is a General Ledger and why is it important?

A General Ledger is a record of a company’s total financial accounts. However, the general ledger definition is much larger than just record keeping.

Since there are multiple accounts recorded in a GL, all of them are independently vital.

The accounts usually recorded in the general ledger are:

- Assets

- Liabilities

- Equity

- Expenses

- Income or Revenue

These are the essential components that you need for efficient financial management.

People often confuse between subledger vs general ledger. While they share the same last name, “ledger”, it doesn’t mean they have identical meanings. It’s quite the opposite, actually.

While a sub-ledger is a comprehensive record of particular transaction types, a general ledger is a detailed overview of an organization’s financial standing and key performance.

Speaking of record keeping of transactions, we will take a slight detour here to look at GL codes.

What is a GL code?

A General Ledger or GL code is a unique alphanumeric string assigned to every financial entry in an organization’s ledger.

Consider this: Your business’ financial transactions are stored in a library. In this case, a GL code acts as the library call number.

That means it has a unique tag attached, which tells you where a specific book belongs and helps you find precisely what you are looking for. That “call number” is what a General Ledger Code is.

General ledger codes are typically used in accounting for classifying and recording every business transaction. These help enterprises record information about purchases, sales, and other transactions.

What else? GL codes show essential information, including debit or credit by location. An example would give you a clearer image. Let’s say there’s a number that reads “GL 531100”. In this case, 5 represents expense transactions, 53 would be operating supplies, 531 is federal supplies, and 5311 refers to office supplies.

Need further help with GL codes?

Talk to Gary, our accounting whiz!

What are the terms of a General Ledger?

To understand a general ledger accounting, you need to understand these nine basic terms and their meanings.

So, here are the key nine terms of a general ledger:

- Accounts: The solo record for each type of asset, liability, revenue, equity and expense.

- Debits and Credits: This is a dual-entry system of accounting that describes an increase or decrease in accounts.

- Chart of Accounts (COA): You can think of COA as an index to your financial books. This is an extensive list of all the services in the general ledger, usually organized by divisions and departments.

- Journal Entries: This is where you store individual records of every transaction. You’ll find all the vital information from the date to the accounts involved.

- Posting: This procedure helps transfer the details from a journal entry to the accounts of a general ledger.

- Trial Balance: This is where you list all the ledger accounts alongside respective debit or credit balances for verifying total debits equal to total credits.

- Fiscal Year: This is the calendar, a 12-month accounting period, that governments and businesses use for financial budgeting and reporting.

- Balance Sheet Accounts: These comprise assets (things the company owns), liabilities (things the company owes), and equity (owner’s share).

- Income Statement Accounts: This is where you record operational transactions, including revenue and expenses.

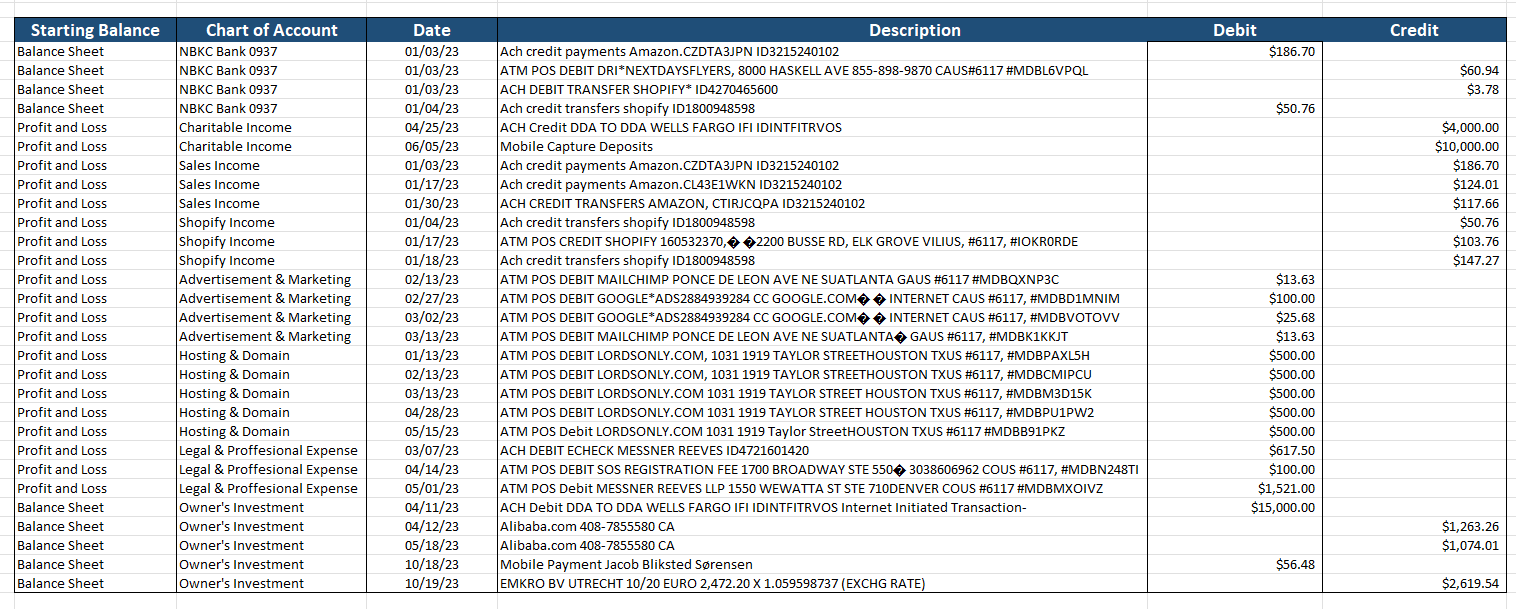

The above terms can be seen in general ledger example that we have added for you.

Notice how the general ledger encompasses all the data required for the 4 types of financial statements: income statement, balance sheet, cash flow statement and statement of equity.

Exploring the different types of General Ledgers

The only way to maintain a comprehensive financial record system is through understanding what general ledger accounting actually is. Further, by understanding the types of General Ledgers we can decide which ones we need.

So, what types of GLs do you need to be aware of? Well, here they are:

1. Traditional General Ledger

This is more like the God of all ledgers because it has been part of accounting for decades now. This is where you keep an eye on transactions manually, entering debits and credits by hand or simple computer programs.

2. Accounts Payable Ledger

This is basically a subset of the general ledger and focuses on the penny your company owes to its suppliers. Know what is accounts payable here in detail.

3. Accounts Receivable Ledger

Converse of the accounts payable ledger, this is where you keep track of the money customers owe your company. This helps big time in predicting future revenue.

4. Tax Ledger

Just as the name suggests, it’s all about taxes. This can help you keep track of all tax-related transactions, ensuring compliance and accuracy.

5. Asset Ledger

From multiple office equipment to patents, the Asset Ledger is where you keep a record of all assets. The best part? This stores everything between depreciation, disposals, and asset management.

6. Expense Ledger

With an expense Ledger, you get a transparent picture of where exactly your money is going. That is because an expense ledger exclusively focuses on keeping a robust record of all the costs incurred by your business.

General Ledger Templates

By now, you would have known that a general ledger is a detailed record of all your financial transactions and account balances. Regarding financial management, a general ledger template can be your ultimate secret ingredient that solves most of your accounting problems.

But what makes an excellent general ledger template?

From customizable and specific to printable and reusable, a template can reduce a solid percentage of your tasks.

This is what general ledger entries should have:

- Account number (if applicable)

- Account name

- Beginning account balance

- Transaction type

- Customer, vendor and employee name in case applicable

- Date

- Debit and credit columns

- Description

Download your customizable General Ledger Template and instantly streamline accounting process!

What is a General Ledger Reconciliation Process?

Now this is where we take you a step further into understanding the general ledger.

Simply put, just as much as knowing what a GL is, is essential, understanding what is general ledger reconciliation is equally important. Get ready because you are about to get a comprehensive rundown on GL reconciliation.

General Ledger Reconciliation is a process accountants use widely to verify the accuracy of account balances stored in a company’s general ledger. This is where you compare the ledger’s contents with the source documents, such as:

- Third-party Data

- Invoices

- Receipts

- Audit reports, bank statements, among other supporting papers

As you would have guessed, reconciliation aims to recognize and rectify discrepancies in the general ledger. Besides preventing errors and discrepancies, it can stop fraud and offer top-notch financial records for cash flow management and better decision-making.

If that’s not enough assurance, we don’t know what is! Truly speaking, nothing can beat the importance of a GL. Furthermore, let’s take a look at best practices of general ledger management that you should keep in mind.

5 Best Practices for General Ledger Management

As we said earlier, GL is the foundation of an organization’s financial reporting system. But, if you don’t know what effective GL management is, you’re one step away from making a big wrong decision. But don’t worry, we’re here for you.

We’ve curated a list of best practices you should definitely go through for managing a general ledger effectively:

1. Get a Clear Chart of Accounts

An organized chart of accounts offers a framework for classifying financial data and maintaining it properly. But remember to review and update it to ensure it aligns with the latest business operations. More clarity on chart of accounts and its types awaits here!

2. Perform Regular Journal Entries

Make it a habit to post journal entries to reflect all financial transactions regularly, including but not limited to revenue, expenses, and asset/liability adjustment.

3. Host Monthly Reconciliation

You must reconcile all General Ledger accounts with external sources, including bank statements, credit card statements, and customer or vendor invoices. The only reason why regular reconciliations are essential is because they help you rectify any discrepancy, avoiding errors that could accumulate with time.

4. Schedule Audits Periodically

This is where you should get an independent auditor to help you conduct periodic audits of the GL to verify whether all data is accurate.

5. Establish Data backup and Security measures

It is very important to have robust data backup and security processes to ensure all sensitive information is safe and not at all in jeopardy.

💡Pro-Tip

Reconciliation can done monthly, quarterly, or yearly. However, we usually recommend that you get it done monthly since it helps catch issues early.

Legal and Compliance Considerations in the U.S.

The Sarbanes-Oxley Act (SOX) of 2002 is a landmark legislation that substantially affected corporate governance and practices related to financial reporting in the U.S. It now has particular implications for general ledger maintenance, focusing more and more on accurate financial records.

This emphasis on accuracy ensures that a strong GL management system can:

- Indicate accurate transaction recording

- Establish internal controls (SOX Section 404) for proper authorization, duty segregation, etc.

- Transparent document processes

- Address unusual transaction

Significance of Generally Accepted Accounting Principles (GAAP)

GAAP acts as the framework to prepare financial statements that are primarily reliable and comparable across different organizations. Adhering to it ensures that the general ledger reflects the company’s financial standing properly, as per the accepted accounting principles.

Bottom Line

Summing up, we can say that a general ledger is basically a GPS. Just as a GPS guides you through unknown places, GL acts as the compass for your business. Simple, right?

From recording every financial transaction to identifying potential pitfalls, it has a solution you need to know. It is more like the backbone of your organization.

Why? Mainly because it gives you a roadmap that helps you make informed decisions. There’s good news if you’ve learned a thing or two reading this. It’s that we have more answers to some of the top questions!

Frequently Asked Questions

1. What is a general ledger account?

A general ledger account, or GL account, is one of the basic elements of financial accounting. It indicates specific groups of financial activity, including assets, liabilities, and revenue/expenses.

2. What does a general ledger look like?

A general ledger almost resembles a T-shaped account with entries on debit and credit sides. While debits show an increase in assets or expenses, credits indicate a decrease in assets (or, often, a boost in liabilities or revenue).

3. What is general ledger reconciliation?

General ledger reconciliation is where you compare the balances of GL accounts with external sources, like bank statements, customer invoices, etc. This process is excellent for identifying errors or discrepancies between the general ledger and the external source.

4. What is the purpose of a general ledger?

The primary purposes of a GL include:

- Tracking financial transactions

- Preparing financial statements

- Maintaining full accuracy

- Ensuring regulatory compliance

- Helps analysis of financial data.

5. What is the general ledger in accounting?

The general ledger, or GL, is the central bank of information for organizations. It is an accounting system that stores financial transactions, like revenue, assets, expenses, and liabilities. It is mainly used to create financial statements.

6. How to record employee retention credit in the general ledger?

The recording of Employment Retention Credit (ERC) is the GL is based on the Accounting method put in place. However, the general approach is when you create a separate GL account for the ERC. Besides, the credit is recorded as a reduction in payroll expenses. The corresponding debit entry is made to a tax receivable or deferred tax liability account.